The Forgotten Privacy Problem in Property Settlements: Who Is Sharing Your Personal Information?

/

Buying or selling property means handing over sensitive personal information. Discover why privacy may be the next major reform issue in conveyancing.

Why privacy matters in conveyancing

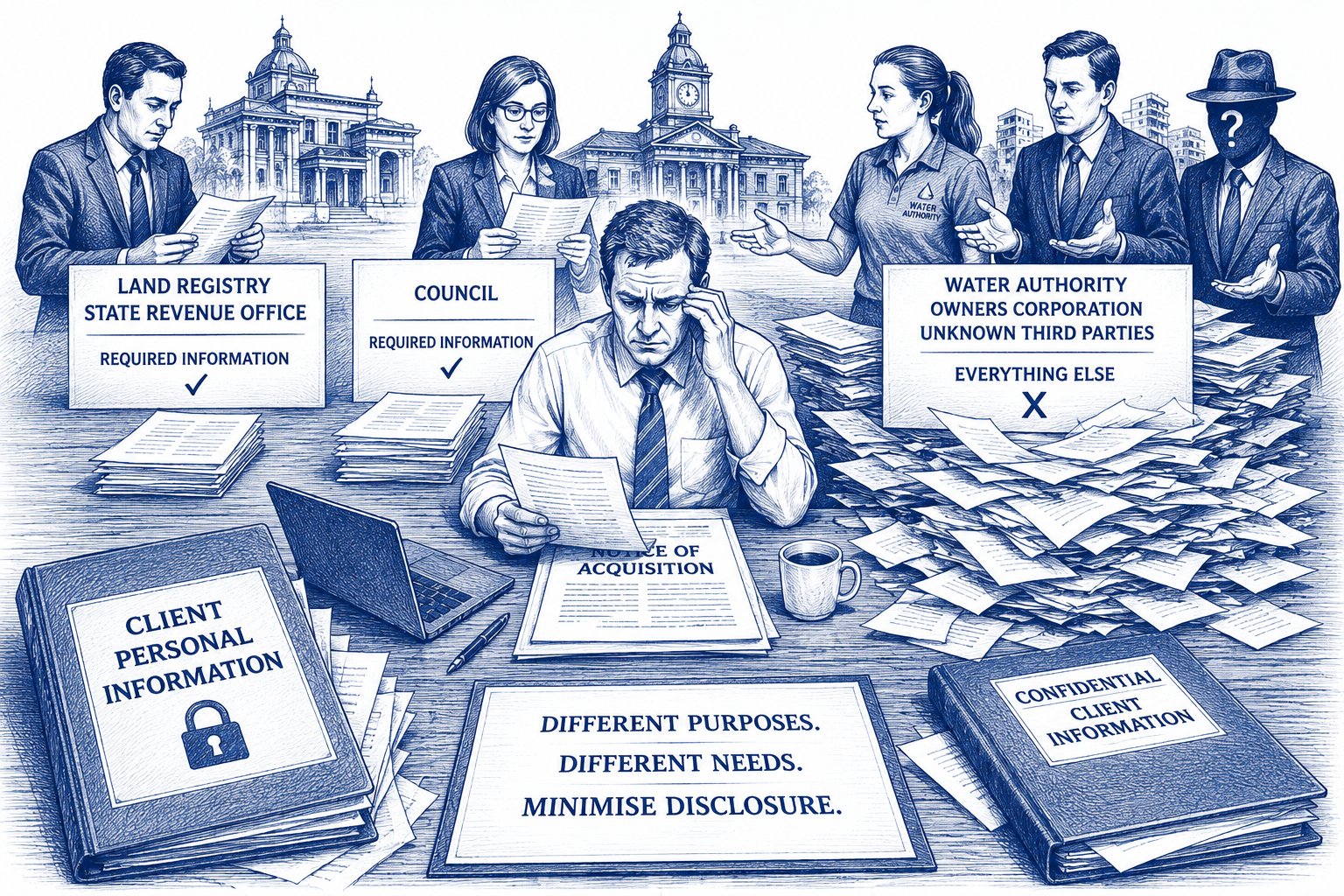

Volume of sensitive data: Property transactions typically require identity documents, tax file numbers, bank details, mortgage information, and sometimes health or family details (for deceased estates or guardianship matters). That data is collected by multiple parties: real estate agents, solicitors, conveyancers, lenders, settlement agents and government registries.

Multiple handoffs increase risk: Each additional party involved raises the chance of accidental disclosure, mishandling or unauthorised access. Files move by email, cloud services, postal mail and in person, often without consistent security standards.

Value to criminals: Personal and financial information from conveyancing files can be used for identity fraud, mortgage fraud, tax crimes and phishing. Property is a high-value target: fraudsters may impersonate buyers, sell properties without owner consent or divert settlement funds.

Regulatory and reputational stakes: Privacy breaches can trigger regulatory action, civil liability and major reputational damage for professionals and firms.

Current weaknesses in the system

Fragmented controls: Different practitioners and agencies operate under varied privacy controls and technologies. Small firms may lack the resources or expertise to implement robust cybersecurity.

Legacy processes: Paper-based exchanges, scanned documents sent by unsecured email and manual verification remain common. These legacy practices are easy to compromise.

Inconsistent identity verification: Proof-of-identity standards vary between participants and jurisdictions, creating gaps that can be exploited by sophisticated fraudsters.

Limited data minimisation: Parties sometimes collect and retain more information than necessary, increasing exposure if a breach occurs.

Cross-jurisdictional complexity: Conveyancing often involves state-based land titles systems and national financial systems, complicating uniform privacy protections.

Why privacy is emerging as a reform issue now

Rising incidence of property-related fraud: Recent years have seen higher rates of title fraud, remote settlement scams and identity theft linked to property transactions. High-profile cases have driven public concern.

Technological change: Digital lodgement, e-conveyancing platforms, cloud storage and electronic settlements increase efficiency but raise new security and governance questions about who controls data and how it’s protected.

Regulatory momentum: Privacy laws, anti-money laundering rules and cyber-security standards are tightening. Policymakers are re-evaluating how these frameworks apply to conveyancing specifically.

Consumer expectations: Home buyers and sellers expect stronger protections for their personal data, especially when transactions are costly and emotionally significant.

Potential reform directions

Mandatory identity verification standards: Uniform, verifiable and auditable ID checks for all parties in a conveyancing transaction (buyers, sellers, agents, settlement officers) to reduce impersonation risk.

Secure data exchange infrastructure: Accredited e-conveyancing platforms with end-to-end encryption, strong access controls and audit trails to replace ad hoc email and paper exchanges.

Data minimisation and retention rules: Clear limits on what information practitioners may collect and how long it can be retained, with secure disposal requirements.

Accreditation and minimum security standards: Mandatory cyber-security baseline (patching, multi-factor authentication, staff training) for conveyancers, agents and settlement agents handling personal data.

Centralised reporting and redress mechanisms: Faster reporting of suspected title or identity fraud to authorities and streamlined remedies for victims (freeze orders, expedited conveyancing checks).

Clarified regulatory responsibilities: Clear allocation of privacy and security obligations across the different actors in a transaction to avoid regulatory gaps and finger-pointing.

Improved public education: Consumer guidance on secure practices (secure document transfer, cheque and funds verification, recognising phishing) and how to verify parties involved.

Practical steps for buyers, sellers and practitioners today

Verify identity in person or by using strong electronic verification methods; don’t rely on unsourced scanned documents.

Use secure file-transfer tools and avoid sending sensitive information by unencrypted email.

Confirm settlement instructions by phone using a known number before transferring funds; be alert for last-minute changes.

Minimise what you provide: only supply documents that are required for the transaction, and ask your practitioner what they will retain and why.

Practitioners should adopt multi-factor authentication, encrypt files at rest and in transit, maintain recent backups, and provide staff training on social engineering.

Keep records of communications and document verification steps in case of a dispute or investigation.

What to watch for next

Reforms are likely to target both technological and procedural weak points: expect new identity standards, accreditation or licensing conditions for e-conveyancing providers, and clearer obligations for data handling.

Insurers and regulators may demand higher cyber-security standards as a condition of professional indemnity or licensing.

Industry consolidation around accredited platforms could reduce exposure from unsecured exchanges but will require robust governance and independent oversight.

Conclusion Conveyancing is inherently data‑intensive